Billing Breakdown: Why You Should Consider an HSA or FSA for ABA Expenses

Katie Sanson

Planning for healthcare expenses is a challenging task for anyone, especially when those expenses come from ongoing and specialized treatment such as ABA therapy.

One way to help plan for healthcare expenses is by enrolling in either an HSA (Health Savings Account) or an FSA (Flexible Spending Account). Both types of accounts are designed to help you save money for eligible healthcare expenses, offering significant tax savings when used.

In this blog, we will cover each type of account, how they differ, and how they can help families who rely on services such as ABA therapy.

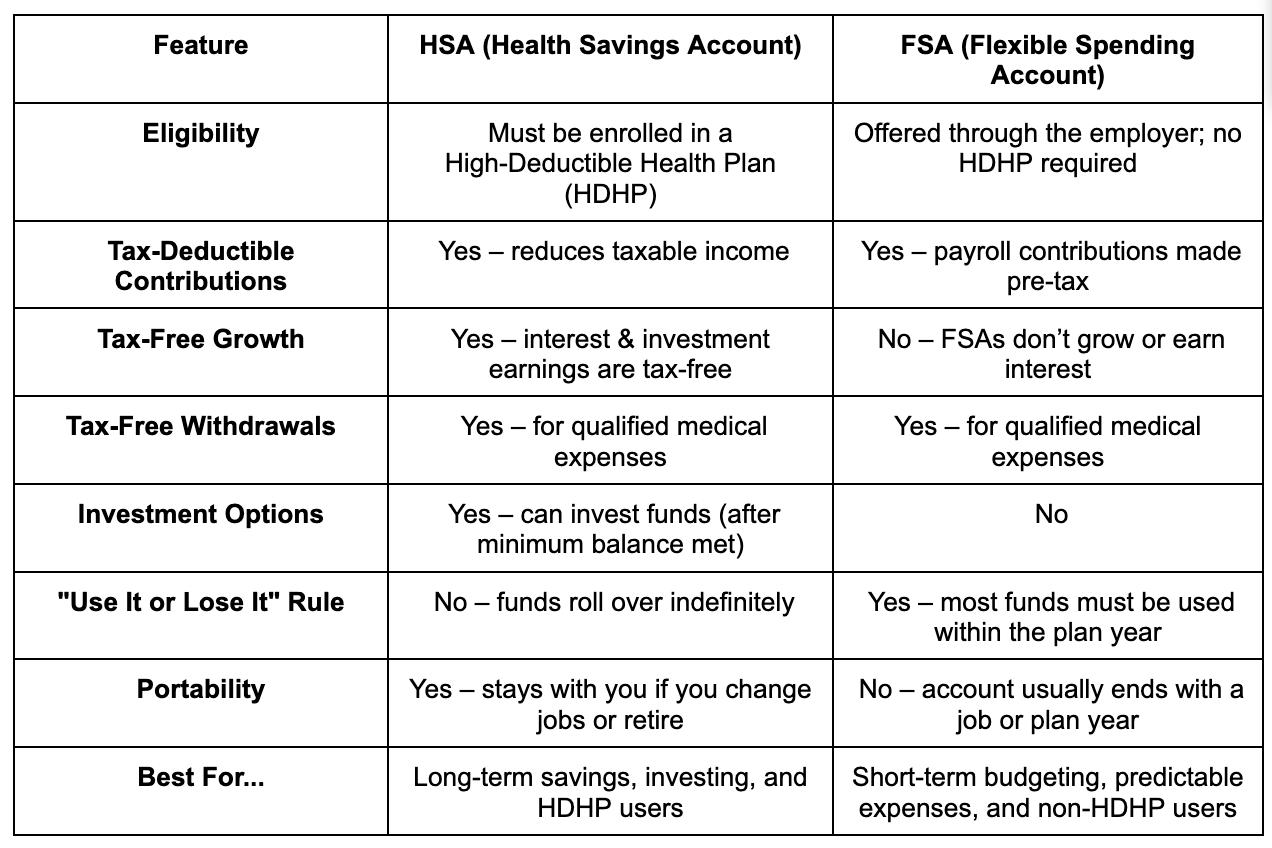

What are HSAs and FSAs?

Both HSAs and FSAs are savings accounts with built-in tax benefits. Money is contributed to these accounts pre-tax, and the funds can then be used to pay eligible out-of-pocket healthcare expenses, such as copays, prescriptions, and dental or vision services, tax-free.

While both accounts can be used towards out-of-pocket costs for ABA therapy, there are a few key differences.

Health Savings Account (HSA)

A Health Savings Account is an option for anyone enrolled in a High-Deductible Health Plan (HDHP). Typically, with an HDHP, you may have a lower monthly premium, but you may need to contribute more out-of-pocket before your health plan pays its portion of costs. By contributing tax-free towards your HSA, money can be set aside to help cover costs associated with the high deductible at the beginning of a plan year.

HSAs are owned by you. Any unused funds at the end of the year are rolled over into the following year and can be transferred to a new employer or health plan.

An additional benefit of Health Savings Accounts is the option to invest a portion of the funds to continue growing the account. Because of the ability to reinvest, HSAs hit the triple threat of tax savings, as not only are contributions and expenses tax-free, but any interest earned or growth from investments is tax-free.

Flexible Spending Account (FSA)

Flexible Spending Accounts (FSA) are only available through employer-sponsored plans. You do not need to be enrolled in a High-Deductible Health Plan to enroll in an FSA, but your employer does need to offer it as an option in your benefits package.

If your employer offers FSA enrollment, the contributions made are still tax-free and can be used tax-free on eligible healthcare expenses. The main difference between FSAs and HSAs is that funds contributed to an FSA do not roll over into the next year and cannot be transferred to a new employer. In other words, it is a “use it or lose it” type of account.

Both HSAs and FSAs have a yearly contribution limit. However, another difference is the inability to reinvest funds once you have reached the contribution limit. This is because the FSA funds do not roll over, and you and the employer partially own the account. Being unable to reinvest simply means the fund is unable to grow via interest earnings.

How Can an HSA or FSA Help with ABA Costs?

Many families receiving ABA therapy will meet their deductible and/or out-of-pocket maximum within the first few months of services due to the intensity and frequency of services. Planning for these costs is critical, and that’s where an HSA or FSA account may come in.

- Reduce Taxable Income:

- Money contributed towards an HSA or FSA is pre-tax, overall lowering your taxable income for the year. Lowering your taxable income could help you see differences in the following year's taxes. With an HSA, you may even be able to grow that balance tax-free.

- Better Budgeting for Expected Healthcare Expenses:

- Either account could be a great option to help grow your savings to use towards healthcare expenses. By funding an HSA or FSA ahead of time, there are funds available immediately to help cover costs, especially if you are enrolled in a High-Deductible Health Plan.

- Cushion for Unexpected Bills:

- Planning for anticipated healthcare expenses is important, but it is also important to prepare for what we cannot anticipate as much as possible. By enrolling in an HSA or FSA, you may be better prepared to help cover the costs of unexpected medical bills after an emergency or accident without needing to dip into other savings or credit options.

Getting Started

To make the most of your HSA or FSA:

- Review your insurance plan to understand your deductible and OOP max.

- Estimate your yearly therapy costs, including copays or coinsurance.

- Check your employer’s benefits portal for enrollment dates and contribution options.

- Ask your ABA provider whether they accept HSA/FSA cards (BPI does!).

Planning for health care expenses for your family doesn’t have to be so challenging. By using an HSA or FSA, you can stretch your dollars further, create a safeguard for future medical expenses, and stress less about out-of-pocket expenses.

If you still have questions on how these accounts work with your current ABA services or insurance plan, please contact us. We are here to help!

Disclaimer: This blog is for informational purposes only and should not be considered financial, tax, or legal advice.

.png)